- Home

- CBSE

- ICSE

- NCERT

- Text Book Solutions

- Our Products

- More

Q.1 What is meant by capital structure?

ANSWER: The proportion of debt and equity used to fund a company’s operations is referred to as its capital structure. In other words, capital structure is the proportion of debt and equity capital in the capital structure. It is difficult to say what type of capital structure is best for a company. The capital structure should be designed to maximize the wealth of equity shareholders by increasing the value of their equity shares. Alphabetically, the Capital structure is Debt Equity Debt Equity or Debt Equity +Debt Debt Equity +Debt.

Q.2 Discuss the two objectives of Financial Planning.

ANSWER: Financial planning entails creating a blueprint for a company’s financial operations. It ensures that the appropriate amount of funds are available for organizational operations at the appropriate time. As a result, it ensures that everything runs smoothly. Firms use financial planning to forecast how much money will be needed at what time, taking into account growth and performance. The two primary goals of financial planning are as follows.

To ensure availability of funds whenever these are required: The primary goal of financial planning is to ensure that sufficient funds are available in the company for various purposes such as the purchase of long-term assets, meeting day-to-day expenses, and so on. It ensures that funds are available on time. In addition to availability, financial planning attempts to specify the sources of finance.

To see that firm does not raise resources unnecessarily: Excessive funding is just as bad as insufficient or scarce funding. If there is a surplus of funds, financial planning must invest it as wisely as possible, as keeping financial resources idle is a significant loss for an organization.

Q.3 What is financial risk? Why does it arise?

ANSWER: Financial risk occurs when a company is unable to meet its fixed financial charges, such as interest payments, preference dividends, and repayment obligations. In other words, it refers to the likelihood of the company failing to meet its fixed financial obligations. It manifests itself as the proportion of debt in the capital structure rises. This is due to the fact that the company is required to pay the interest charges on debt in addition to the principal amount. As a result, the greater the debt, the greater the payment obligations, and thus the greater the chances of payment default. As a result, increased use of debt entails increased financial risk for the company.

Q.4 Define a ‘current asset’. Give four examples of such assets.

ANSWER: Current assets are assets that are retained in the business with the intention of converting them anytime into cash within a short period of time i.e. one year. For example, goods are purchased with the intent of reselling them and earning a profit, debtors exist to convert them into cash, i.e., receive the amount from them, and bills receivable exist to receive cash against them. Current assets include short-term investments, debtors, stocks, and cash equivalents.

Q.5 Financial management is based on three broad financial decisions. What are these?

ANSWER: Financial management is the efficient acquisition, allocation, and utilization of a company’s funds. It focuses on three major aspects of financial decisions: investment decisions, financial decisions, and dividend decisions.

1. Investment decisions include the purchase of fixed assets (called capital budgeting). Investment in current assets is also a type of investment decision that is referred to as a working capital decision.

2. Financial decisions – They concern the raising of funds from various sources, which will be determined by the decision on the type of source, the period of financing, the cost of financing, and the resulting returns.

3. Dividend decision – The finance manager must make a decision on net profit distribution. Net profits are typically divided into two categories:

1. Dividend for shareholders- A dividend, as well as the rate at which it will be paid, must be determined.

2. Retained profits- The amount of retained profits must be finalized, which will be determined by the enterprise’s expansion and diversification plans.

Q.6 What are the main objectives of financial management? Briefly explain.

ANSWER: Financial management is generally concerned with the procurement, allocation, and control of a company’s financial resources. The goals could be

Q.7 How does working capital affect both the liquidity as well as profitability of a business?

ANSWER: A company’s working capital is defined as the excess of current assets (such as cash on hand, debtors, stock, and so on) over current liabilities. Working capital has an impact on a company’s liquidity as well as its profitability. The liquidity of the business increases as the amount of working capital increases. However, because current assets provide a low return, increasing working capital reduces business profitability. For example, increasing the business’s inventory increases its liquidity, but because the stock is kept idle, the profitability falls. Low working capital, on the other hand, impedes the day-to-day operations of the business. As a result, working capital should be allocated in such a way that a balance between profitability and liquidity is maintained.

Q.1 What is meant by working capital? How is it calculated?

Discuss five important determinants of working capital requirements.

ANSWER: Working capital is that part of total capital which is required to H meet day-to-day expenses, to buy raw materials, to pay wages and other

expenses of routine nature in the production process or we can say it refers 2 to excess of current assets over current liabilities.

Working Capital = Current Assets – Current Liabilities

Factors affecting working capital requirement are

2 (i) Nature of Business The basic nature of a business influences the

amount of working capital required. A trading organisation usually needs a lower amount of working capital compared to a manufacturing organisation. This is because in trading, there is no processing required. In a manufacturing business, however, raw materials need to be converted into finished goods, which increases the expenditure on raw material, labour and other expenses,

(ii) Scale of Operation The firms which are operating on a higher scale of operations, the quantum of inventory, debtors required is generally high, Such organisations, therefore, require large amount of working capital as compared to the organisations which operate on a lower scale.

(iii) Production Cycle Production cycle is the time span between the receipts of raw materials and their conversion into finished goods.

Some businesses have a longer production cycle while some have a shorter one. Working capital requirement is higher in terms with longer processing cycle and lower in firms with shorter processing cycle.

(iv) Credit Allowed Different firms allow different credit terms to their customers. A liberal credit policy results in higher amount of debtors, increasing the requirements of working capital.

(v) Credit Availed Just as a firm allows credit to its customers it also may get credit from its suppliers. The more credit a firm avails on its purchases, the working capital requirement is reduced.

Q.2 Capital structure decision is essentially optimisation of risk-return relationship. Comment.

ANSWER: Capital structure refers to the mix between owners and borrowed funds. It can be calculated as Debit/Equity.

Debt and equity differ significantly in their cost and riskiness for the firm. Cost of debt is lower than cost of equity for a firm because lender’s risk is lower than equity shareholder’s risk, since lenders earn on assured return and repayment of capital and therefore they should require a lower rate of return. Debt is cheaper but is more risky for a business because payment of interest and the return of principal is obligatory for the business. Any default in meeting these commitments may force the business to go into liquidation. There is no such compulsion in case of equity, which is therefore, considered riskless for the business. Higher use of debt increases the fixed financial charges of a business. As a result increased, use of debt increases the financial risk of a business.

Capital structure of a business thus, affects both the profitability and the financial risk. A capital structure will be said to be optimal when the proportion of debt and equity is such that it results in an increase in the value of the equity share.

Q.3 A capital budgeting decision is capable of changing the financial fortune of a business. Do you agree? Why or why not?

ANSWER: Investment decision can be long term or short term. A long term investment decision is also called a capital budgeting decision. It involves commiting the finance on a long term basis, e.g., making investment in a new machine to replace an existing one or acquiring a new fixed assets or opening a new branch etc. These decisions are very crucial for any business. They affect its earning capacity over the long-run, assets of a firm, profitability and competitiveness, are all affected by the capital budgeting decisions. Moreover, these decisions normally involve huge amounts of investment and are irreversible except at a huge cost. Therefore, once made, it is almost impossible for a business to wriggle out of such decisions. Therefore, they need to be taken with utmost care. These decisions must be taken by those who understand them comprehensively A bad capital budgeting decision normally has the capacity to severely damage the financial fortune of a business.

Q.4 Explain factors affecting the dividend decision.

ANSWER: Dividend decision relates to distribution of profit to the shareholders and its retention in the business for meeting the future investment requirements.

How much of the profits earned by a company will be distributed as profit and how much will be retained in the business is affected by many factors. Some of the important factors are discussed as follows

(i) Earnings Dividends are paid out of current and past year earnings. Therefore, earnings is a major determinant of the decision about dividend.

(ii) Stability of Earnings Other things remaining the same, a company having stable earning is in a position to declare higher dividends. As against this, a company having unstable earnings is likely to pay smaller dividend.

(iii) Growth Opportunities Companies having good growth opportunities retain more money out of their earnings so as to finance the required investment. The dividend in growth companies, is therefore, smaller than that in non-growth companies.

(iv) Cash Flow Position Dividends involve an outflow of cash. A company may be profitable but short on cash. Availability of enough cash in the company is necessary for declaration of dividend by it.

(v) Shareholder Preference If the shareholder in general, desire that at least a certain amount should be paid as dividend, the companies are likely to declare the same.

(vi) Taxation Policy If tax on dividend is higher it would be better to pay less by way of dividends. As compared to this, higher dividends may be declared if tax rates are relatively lower.

(vii)Stock Market Reaction For investors, an increase in dividend is a good news and stock prices react positively to it. Similarly, a decrease in dividend may have a negative impact on the share prices in the stock market.

(viii) Access to Capital Market Large and reputed companies generally have easy access to the capital market and therefore, depend less on retained earnings to finance their growth. These companies tend to pay higher dividends than the smaller companies which have relatively low access to the market.

(ix) Legal constraints Certain provisions of the Company’s Act place restriction on payouts as dividend. Such provisions have to be adhered, while declaring dividends.

(x) Contractual Constraints While granting loans to a company, sometimes the lender may impose certain restrictions on the payment of dividends in future. The companies are required to ensure that the dividends does not violate the terms and conditions of the loan agreement in this regard.

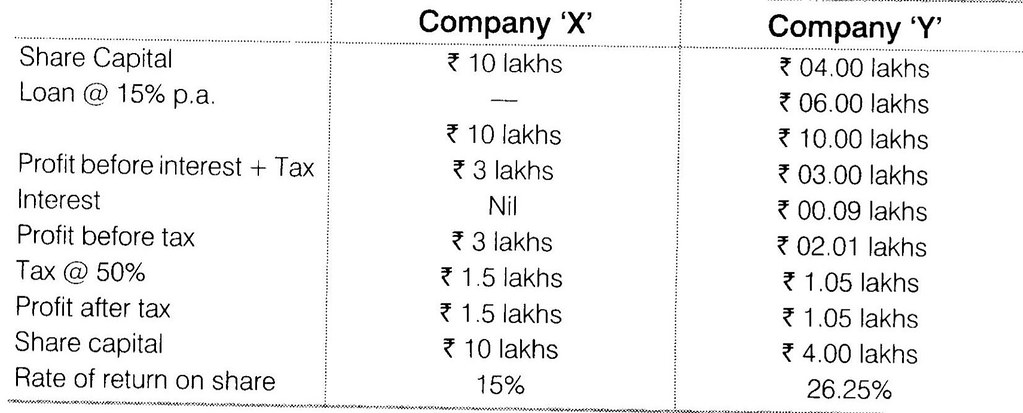

Q.5 Explain the term ‘trading on equity’. Why, when and how it can used by a business organisation?

ANSWER: Trading on equity refers to the increase in profit earned by the equity shareholders due to presence of fixed financial charges. When the rate of earning or Return on Investment (ROI) of a company is higher than the rate of interest on borrowed funds only then a company should opt for trading on equity. Let us consider the following example

It should be clear from the above example, that shareholders of the company ‘X’ have a higher rate of return than company ‘Y’ due to loan component in the total capital of the company.